Do You Take Installments: A Practical Guide for Homeowners and DIYers

Learn how installment options work for home projects, compare terms, and apply confidently. A data-informed guide by Install Manual for homeowners and DIYers.

The short answer is yes—many retailers and contractors offer installment options or financing to help spread the cost of installation projects. Terms vary, with some promos offering 0% APR and others showing fixed monthly payments over several months. This guide explains how installment options work, how to compare offers, and practical steps to apply.

Why the question do you take installments matters for home projects

For homeowners and DIYers, the common question do you take installments often determines whether budget constraints delay or derail a project. Budget planning for installations—like a new dishwasher, water heater, or upgraded HVAC components—can hinge on whether you can spread payments over time. The Install Manual team has observed that installment options are especially valuable when a project requires high upfront costs but promises long-term energy or reliability benefits. When you ask a retailer or contractor if they take installments, you’re not just negotiating price—you’re negotiating cash flow for the project timeline. If you decide to pursue installments, you’ll want to understand the term lengths, any promotional rates, and how payments align with your household budget. This article will guide you through evaluating offers and choosing the option that minimizes total cost while maintaining project quality.

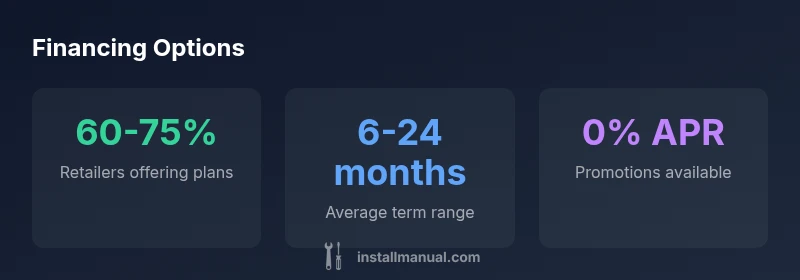

How installment options work with installation projects

Installment options typically break the total project cost into scheduled payments. Common structures include 6, 12, 18, or 24 month terms, sometimes with a 0% APR promotional period that applies if you meet on-time payment requirements. After a promotional window, the rate reverts to the standard APR. Some offers are tied to the retailer or service provider, while others come from third-party lenders. When you sign an installment agreement, you’re agreeing to a fixed payment schedule and a total payoff amount. Important nuances include whether there are late fees, the impact of missed payments on credit, and whether early payoff is allowed without penalties. Always read the terms closely and confirm how the project timeline aligns with the payment schedule. For DIYers, this can mean financing a larger appliance install or HVAC upgrade with payments that fit seasonal budgets.

When to choose installments vs upfront payment

Choosing installments versus paying upfront depends on several factors. If your cash flow is tight but the project’s value justifies the expenditure, installments can prevent delays and allow you to begin work sooner. However, if you can secure a favorable upfront price or a lender with a very low total cost, paying upfront might save money in the long run. Consider the following decision triggers: (a) urgency of the project (can you wait for a promo period?), (b) total cost including interest and fees (is the effective rate worth the convenience?), (c) impact on your credit score (will a new loan affect your debt-to-income ratio?), and (d) the reliability of the contractor or retailer (do they honor promotions and provide clear payoff terms?). The goal is to minimize total cost while preserving project quality and timing. Install Manual notes that many homeowners find installments helpful for larger projects that improve energy efficiency or safety, provided they actively compare offers and plan real budget implications.

How to evaluate terms and avoid traps

Before accepting any installment offer, perform a quick, disciplined evaluation. Key steps include: (1) compare the total cost across offers, not just monthly payments; (2) check promotional APR windows and whether any balance accrues interest during the promo; (3) identify any hidden fees (origination, late payment, or early payoff penalties); (4) confirm the eligibility criteria and required documents; (5) verify whether the contractor or retailer is upfront about project milestones and payment timing; and (6) ensure the agreement aligns with your project schedule. A good rule of thumb is to calculate the worst-case total cost if you miss a payment and to verify there is no prepayment penalty if you plan to finish early. The Install Manual approach emphasizes transparent terms, written promises, and a clear path to payoff. By comparing multiple offers, you reduce the risk of overpaying in service fees or interest.

Step-by-step guide to applying for an installment plan

- Define the project scope and budget, including all ancillary costs. 2) Gather documents (proof of income, residency, ID, and perhaps a recent credit report). 3) Check whether the contractor offers an in-house plan or directs you to a third-party lender. 4) Compare at least two offers, focusing on the total cost and monthly payment impact. 5) Pre-qualify with soft pulls to avoid affecting your credit score. 6) Choose the option with the lowest total cost that fits your budget, and ensure you have a clear written agreement detailing milestones and payments. 7) Confirm work start dates and payment triggers tied to project progress. 8) Maintain organized records of all receipts and communications to resolve disputes quickly. The intent is to move from initial inquiry to an informed, written agreement that protects both your budget and the project timeline.

Alternatives and cautions for DIY buyers

If installment plans aren’t suitable, consider alternatives such as a savings-based approach, a credit card with a temporary 0% APR promo, or a personal loan with a fixed rate and predictable payoff. For some projects, layaway or a delayed-start plan might allow you to accumulate funds while securing savings or promotions on the necessary equipment. However, be mindful of high-interest rates, annual fees, or promotional periods that require perfect payment punctuality. Always balance convenience with total cost and ensure that the financing aligns with your broader household budget. Install Manual encourages homeowners to explore every option, verify all terms in writing, and choose the option that minimizes financial stress while preserving project quality.

Practical tips and planning checklist

- Start with a 3-bucket budget: upfront cost, monthly payments, and contingency.

- Ask for written terms and confirm all fees upfront.

- Use a calculator to estimate total payoff under worst-case scenarios.

- Prioritize options that offer transparent, fixed payments and no prepayment penalties.

- Keep a calendar of due dates to avoid late fees.

- When possible, select plans with clear milestones that tie payments to work completed.

- Revisit the plan after the project starts to adjust if needed and avoid being locked into unfavorable terms.

Comparison of financing options for home installation projects

| Financing Option | Typical Terms | Pros | Cons |

|---|---|---|---|

| Retailer installment plan | 6–24 months; promotional 0% APR periods possible | Convenient; often no upfront cash | Interest or fees may apply after promo; eligibility checks |

| 0% APR credit card | Promotional 0% APR for 6–18 months; standard rate after | Widely accepted; may earn rewards | Requires good credit; potential higher rates later; annual fees |

| Personal loan | Fixed-rate loan over 2–5 years | Predictable payments; clear total cost | Interest costs; affects credit utilization |

| Layaway / reserve-in-advance | Pay upfront in installments; item held | No debt; price protection | Limited availability; longer wait for project start |

Got Questions?

Do you take installments for installation services?

Yes. Many installers and retailers offer installment plans or financing to spread the cost of installation services. Eligibility and terms vary by provider, and it’s important to compare total cost rather than just the monthly payment.

Yes, many installers offer installment plans. Eligibility and terms vary, so compare total costs and pick the option that fits your budget.

What is the typical qualification process for an installment loan?

Expect a standard credit check, income verification, and proof of residence. Some plans use soft credit pulls initially. Be prepared with recent pay stubs, ID, and banking details.

Most plans require a credit check and income verification. Have your pay stubs and ID ready.

Are installment plans always the best option?

Not always. If you can secure a low total cost with upfront payment or a short-term loan with favorable terms, installments may not be necessary. Consider project urgency, total cost, and budget impact.

Not always. Compare total costs and terms to decide if installments are right for you.

How should I compare offers effectively?

Look at APR, promotional period length, all fees, repayment schedule, and any penalties for late payment or prepayment. Compute the total cost over the life of the plan.

Compare APR, fees, and total cost, not just monthly payments.

Can I negotiate terms with the retailer or lender?

Yes. You can often negotiate interest rates, promotional periods, or repayment schedules. Asking for a match with a rival offer can also help secure better terms.

Yes—negotiate rates, promo periods, and repayment options when possible.

“Financing for home projects should be treated as a budgeting tool, not a surprise cost. Always compare terms and total cost.”

Main Points

- Define your project budget before choosing options.

- Compare total costs, not just monthly payments.

- Check eligibility and required documents early.

- Beware promo APR traps and upfront fees.

- Ask for written terms and clear payoff options.